Current ADA liquidity pools are set as ‘volatile’ assets, meaning it is cheaper to take out loans before reaching the optimal utilization rate of 45%. Take the ADA/LENFI pool as an example.

In this scenario, borrowers are unlikely to take new loans due to high interest rates, while depositors receive relatively low yields since active loans are not costly.

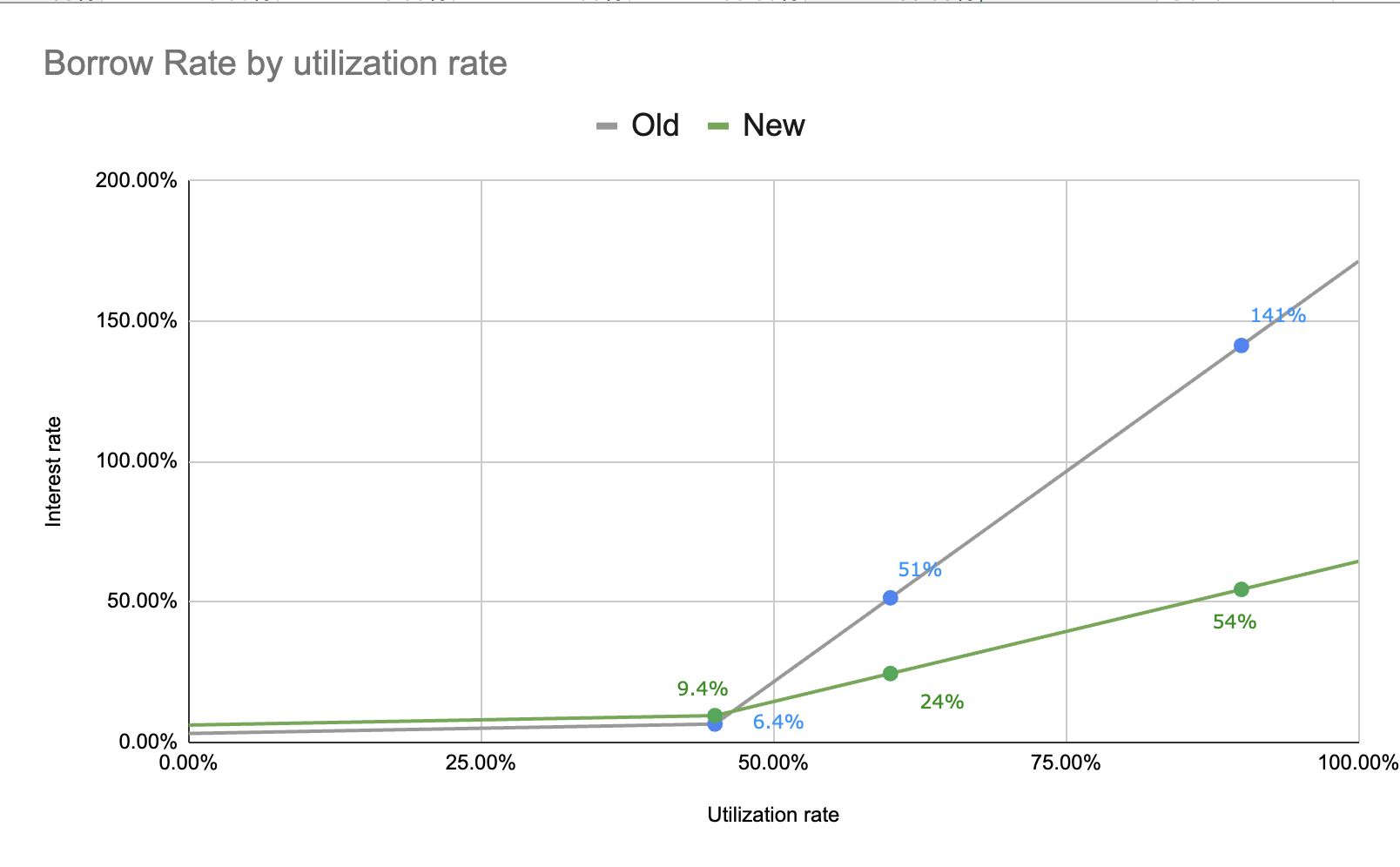

The pool has the following parameters:

Optimal utilization rate: 45%

Base interest rate: 3%

Slope1: 7.5%

Slope2: 300%

These parameters deter borrowers from taking out new loans as the cost increases significantly.

I propose opening a discussion to increase the base interest rate to 6% and reduce Slope2 to 100% for ADA supply pools.

This adjustment would result in:

Loans becoming more expensive when the utilization rate is low.

Loans remaining costly when the utilization rate exceeds the optimal rate, but not excessively so.

To illustrate, here are the changes in the current pool rates:

This modification should lead to higher supply rates when utilization has not reached optimal levels and lower rates after surpassing the optimal rate.

However, this might result in higher utilization rates, potentially making it more challenging for liquidity providers to withdraw assets.

It would be great if we had data on other protocols to compare and contrast with on the graph you’ve shared. It’s still early days for V2 and trust and value for money is still being built.

I’m all for lowering slope 2, however the 3% increasing to 6% I’m slope 1 I’d need to see more data points for on how it compares against other lending protocols not just our own.

So for Ada I think I agree with the proposal as is and would be happy to vote for it.

Is it worth also thinking about stables (or at least some of them) being treated the same way as the Ada in this proposal? Not sure how some of the pegs are doing at the moment

I love it! The 6% base rate is great. The only thing I’d do differently is make the slope1 and optimal utilization rate bigger. Maybe 10 to 12 on Slope1 and 65 on optimal utilization rate. This would allow more of the pool to be accessed by borrowers and allow a higher rate for suppliers. Accessing more of the supply may be the most important. A borrower has to be really desperate to drive the utilization past 50% right now.

An even more optimal solution would be to use the V1 data to allow the parameters to be different for different pairs.

But, it’s a great proposal and it should increase the supplier rates.

absolutly perfect we definatly need these fee system and also the locking of lenfi to earn and protect the protocol, vote… if token holders can earn protocol fees and liquidation fees along with interest at a balance rate this is massive incentive to also hold the lenfi token because people will have a massive reason… so mantas you the boss and if you realise its the same thing we all been talking about… so we see the problem and know the solution.

I looked at various parameters in the spreadsheet with the goal of increasing the funds available between 10 and 15 percent (thinking mainly Lenfi/ada pool). I think that is what is missing in getting the lender rates higher

Our current settings (3% base, 45% util, 7.5 slope1, and 300 slope2) has a 1% range for loans with rates between 10 and 15. We hit 10% rate at 47% util and hit 15 at 48% util.

Using the Mantas suggested parameters (6 base, 45 u, 7.5 s1, and 100 S2) increases that range to 5% of the funds (hit 10 at 46 u and 15 at 51 u).

Using parameters like these (6 base, 65 u, 12 s1, and 100 S2) increases the range to 30%. We start 10% loans at 33% util and hit 15 at 66% util. That means if we get to the optimal utilization number (65%), then half of the supply would have been loaned at rates between 6 and 10 percent and half between 10 and 15. That’s going to give us a supplier rate of around 10%, which should be high enough to attract ADA deposits. This is a much better and sustainable way to attract deposits than giving out incentives.

sweet so can we say this interest rate is now sorted and you can work on things like buyback mechanics… and safetypool because Approach for a Safety Module proposal is spot on along the lines of what you were also thinking all you would and tam would need to do is add whats missing and get it up and running

Would the rate change for existing borrowers as utilization changes? Similar to Aave? Or would the interest rate stay the same, set initially when the borrower opens the loan and is fixed for the term of the loan.

Thanks. My fear is 6% base may still be too low, especially in this market. The ability to lend > borrow > withdraw means large users can consistently get access to the base rate.

Makes sense. I didn’t mean to state I don’t think this proposal helps. I 100% believe this proposal helps and I commend you for it. My personal opinion is the base rate may still be too low at 6. But this is a step in the right direction.